Can we live our lives without caring much about our personal finance? The answer is no! The decisions we make as touching our personal finance is a sum total of our behavior. Personal finance as it were is connected to behavior because our habits, opinions, and psychological makeup have a significant impact on our financial decisions.

It’s an obvious fact that our unique behaviors and decision-making processes influence how we manage our personal finance, from saving and investing to spending and creating a budget. Knowing this relationship is crucial because it helps explain why some people succeed and attain financial stability while others face difficulties. Better financial results can be achieved by developing healthier personal finance habits and making more informed judgments by acknowledging and correcting the behaviors that influence our financial choices.

In this article, why is personal finance dependent upon your behavior? I’ll be exploring the answer and 8 key factors that best explore this pertinent question.

Let’s dive in

1.1. Why Is Personal Finance Dependent Upon Your Behavior?

Personal finance depends on your behavior because your financial decisions are driven by habits, emotions, and discipline. How you spend, save, invest, or manage debt, are mostly dependent on your behavior. Setting goals, maintaining consistency, and exercising self-control are all necessary for effective money management. These are behavioral traits. You make wiser financial decisions, stay out of debt, and work toward your financial objectives by controlling your behavior.

1.2 Importance of Personal Finance

The importance of personal finance is undisputable, it’s as important as monitoring your blood pressure monthly. Not only that, understanding and managing personal finance is crucial for achieving financial well-being and security. However here’s why personal finance is so important:

- Financial Stability: Your capacity to manage money well and maintain stability is aided by personal finance.

- Future Security: Personal finance enables you to save and makes it possible for you to invest in gainful ventures.

- Effective Budgeting: Budgeting is the act of planning your expenses, thus personal finance allows you to budget wisely, balancing income and expenses.

- Debt Avoidance: You can’t go into unnecessary debts when you have a strong control over personal finance.

- Emergency Preparedness: Personal finance eases your financial strain by preparing you for unforeseen costs.

- Wealth Building: Personal finance helps to cultivate good financial habits that lead to wealth creation over time.

- Improved Quality of Life: Proper personal finance management enhances your overall quality of life.

- Freedom to Pursue Goals: Personal finance gives you the freedom to pursue your personal aspirations and life goals.

- Long-Term Well-Being: Mastering personal finance is the gate way to achieving long-term financial health.

1.3 Influence of behavior on financial decisions

While financial decisions may appear to be entirely rational, they are frequently greatly influenced by behavioral elements. The influence of behavior on financial decisions refers to how our thoughts, emotions, habits, and psychological biases determine the way we manage and interact with money.

1. Behavioral Economics: This branch of study shows that due to biases like overconfidence, delay, or fear of loss, we frequently make personal finance decisions that are not necessarily in our best interests. For instance, despite the possibility of long-term financial growth, we may choose not to invest in stocks because of a fear of losing money.

2. Emotional Factors: Our personal finance decisions can be influenced by emotions such as fear, greed, joy, or stress. For instance, we may resort to “retail therapy” as a way to alleviate an emotional state, or we may panic-sell stocks during a market downturn, which could result in losses.

3. Cognitive Biases: Our financial decisions can be influenced by biases like confirmation bias, which favors information that supports preexisting ideas, or status quo bias, which favors maintaining the status quo. These biases frequently causes us to make irrational or suboptimal judgments, such as adhering to antiquated personal finance tactics or passing up fresh investment chances.

4. Habitual Behavior: Frequent financial behaviors, such as persistent overspending or budgeting insufficiently, form habits that can support or undermine sound financial management. By comprehending these behaviors, we can spot trends that might be harmful to our financial stability.

The influence of behavior on our finances can never be overestimated however by being able to identify the psychological influences at work in our personal finance and devise techniques to make more logical, advantageous selections we can manage our money more wisely, steer clear of common financial mistakes, and work toward our financial objectives more successfully by becoming aware of our biases and emotional triggers.

2. The Psychology of Personal Finance

The psychology of personal finance studies the mental and emotional drivers behind the choices we make with our money as earners. Understanding the actions, feelings, and cognitive biases that influence our financial decisions is just as important as knowing how much money we make or save.

Through an analysis of behavioral economics, we can observe how biases like overconfidence and procrastination, as well as emotions like enthusiasm and fear, have a direct impact on how we handle our finances. To create better financial habits, make wiser choices, and achieve long-term financial stability, it is imperative to comprehend these psychological factors:

2.1 Key principles of behavioral economics in finance

1. Loss Aversion: This can result in unduly conservative decisions because it is human nature to dread losses more than to value comparable rewards.

2. Overconfidence Bias: An act of overestimating one’s own financial knowledge and capability, which frequently results in taking unwarranted risks.

3. Mental Accounting: When we treat money differently based on its source or intended use, affects our spending and saving behaviors.

4. Herd Behavior: The conscious or unconscious act of following the crowd, which can lead to market bubbles or crashes.

5. Present Bias: Favoring short-term profits over long-term ones; this tendency frequently leads to delay and reckless spending.

6. Status Quo Bias: When we prefer the status quo and opposing change can keep you from making the best financial decisions.

2.2 How emotions and cognitive biases affect financial choices

Here are the ways, financial decisions are greatly influenced by your emotions and cognitive biases:

- Emotions

- Fear: An excessively cautious approach to investing due to the fear of losing money can result in the loss of potentially profitable chances. For instance, fearing that your investments will be locked in, may lead you to sell your equities during a market downturn.

- Greed: When you chase after the newest “hot” stock or take excessive risks in your investments, it can lead to significant financial losses. This is because you are motivated by a desire for large returns.

- Guilt: According toWikipedia Guilt is a moral emotion that occurs when a person believes or realizes accurately or not that they have compromised their own standards of conduct. Feeling guilty about past financial mistakes can lead to restrictive behaviors, such as cutting back on necessary spending or avoiding making new investments, which might hinder your financial growth.

- Joy: Most times Positive emotions, like excitement can be a driving force that can propel you to impulsive spending or poor investment decisions, such as splurging on luxury items rather than saving or investing.

- Cognitive Biases

- Overconfidence Bias: We often overestimate our financial knowledge and abilities, leading to risky investments or poor financial planning based on the belief that we can consistently beat the market.

- Confirmation Bias: Sometime we tend to seek out information that supports our existing beliefs and ignore contrary evidence. For instance, we may read news that confirms our positive outlook on a particular stock while disregarding negative reports.

- Anchoring: Your firsthand knowledge or pointers have a significant impact on choices. If you purchases a stock, for instance, at $100, you could tend to hold onto it and not want to sell it, even if its value drops dramatically.

- Mental Accounting: We make less-than-ideal financial decisions when we divide our income into several “buckets” (such as savings, expenditures, and investments). For instance, instead of investing a tax refund, we perceive it as “extra” money which could lead to wasteful consumption.

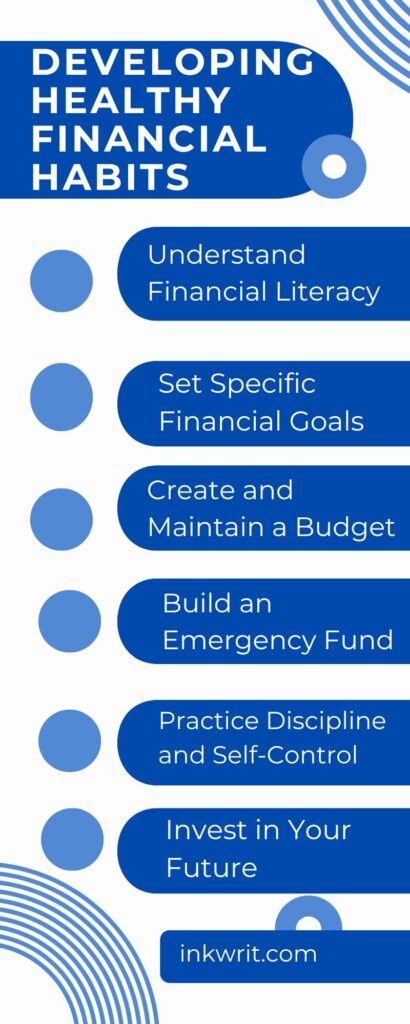

3. Developing Healthy Financial Habits

Long-term financial security and confidence can only be attained by developing sound financial habits. These practices make it easier for you to plan ahead, manage your finances, and deal with unforeseen expenses. The following are the six essential steps to forming healthy money practices:

1. Understand Financial Literacy

“The reason that the rich were so rich, Vimes reasoned, was because they managed to spend less money. Understanding how finance literacy plays is crucial to an effective money management system. Key concepts like basic budgeting, saving, investing, and debt management are what engineers a healthy financial habits. The more knowledgeable you are about these things, the better equipped you are to make sound decisions that prevent costly mistakes and help you reach your financial goals.

2. Set Specific Financial Goals

Having specific financial goals helps you stay motivated and provides you with something to strive for. Your financial decisions and behaviors are guided by having specific, measurable, attainable, relevant, and time-bound (SMART) goals, whether you’re saving for a down payment on a house, organizing a trip, or getting ready for retirement. By reviewing these objectives on a regular basis, you can make necessary adjustments and stay on course.

3. Create and Maintain a Budget

One essential tool for managing your finances is a budget. It assists you in keeping tabs on your earnings and outgoings, pinpointing areas for cost reduction, and allocating money for investments and savings. Making a budget that aligns with your financial objectives and checking it frequently will help you make sure you are living within your means and making progress toward your goals.

4. Build an Emergency Fund

An emergency fund offers a safety net in case of unforeseen circumstances like auto repairs, medical difficulties, or job loss. Your goal should be to accumulate three to six months’ worth of living expenditures in an easily accessible, separate account. Establishing this money can ease anxiety, avoid debt, and offer piece of mind.

5. Practice Discipline and Self-Control

Sustaining sound financial practices requires self-control and discipline. This entails adhering to your budget, avoiding impulsive purchases, and making thoughtful financial decisions. You can stay dedicated to your financial goals, avoid needless debt, and save regularly by adopting a disciplined approach to money management.

6. Invest in Your Future

The secret to increasing your wealth over time is investing. It is essential to comprehend various investing possibilities, such as stocks, bonds, mutual funds, and real estate, and how they align with your objectives and risk tolerance. For maximum earnings and financial security, start small, diversify your portfolio, and seek professional counsel as necessary.

3.1 The significance of financial literacy in money management.

Your overall financial well-being and efficient money management depend on having a solid understanding of finance. Comprehending and utilizing fundamental financial principles is necessary to arrive at well-informed financial situation. These are some of the reasons why financial literacy is so important:

1. Informed Decision-Making

Financial literacy provides you with the information necessary to make wise financial decisions. Whether you’re comparing savings accounts, analyzing loan offers, or selecting investments, knowing the meaning of financial terms and concepts will help you weigh your options and determine which is best for you.

2. Effective Budgeting

You can make and stick to a reasonable budget if you have a firm understanding of financial concepts. You can handle your finances more skillfully if you know how to track income, classify expenses, and set spending restrictions. This can help you stay under budget and make sure that your resource allocation matches your financial objectives.

3. Debt Management

Understanding various forms of debt, including credit card debt, student loans, and mortgages, as well as how to manage them, is made easier with financial literacy. Making informed decisions about borrowing and debt repayment helps you stay out of financial difficulty by providing you with knowledge about interest rates, payment conditions, and credit scores.

4. Saving and Investing

You can make more informed choices about investing and saving money if you have a solid foundation in financial literacy. You can make plans for both short-term necessities and long-term objectives, like retirement, by being aware of the concepts of compound interest, risk versus return, and various investment vehicles, including stocks, bonds, and mutual funds.

5. Financial Planning

Effective financial planning requires financial literacy. It helps you to make necessary adjustments to your plans and to define realistic financial goals and tactics to attain them. Financial literacy enables you to make and stick to a plan that supports your goals, whether you’re saving for a child’s college education, making a large purchase, or getting ready for retirement.

6. Protecting Against Fraud

Having a firm grasp of financial principles enables you to identify and steer clear of possible financial fraud and scams. Being aware of how financial institutions function, recognizing warning signs, and safeguarding personal data lessens the likelihood of becoming a victim of financial scams.

7. Promoting Financial Security

Finally, by helping you to handle your money wisely, financial literacy advances financial security. It aids in responsible debt management, emergency fund building and maintenance, and prudent saving and investment decisions. In addition an increased peace of mind, a better quality of life, and less stress can result from having financial security.

3.2 Practical tips for cultivating positive financial behaviors

The secret to obtaining and preserving financial health is to cultivate sound money habits. To assist you in creating and maintaining these sound habits, consider the following helpful advice:

1. Automate Savings

Establish automated transfers to a savings or investment account from your checking account. By automating your savings, you can make sure that you consistently make contributions to your financial objectives without having to remember to make manual transfers. Set aside a certain portion of your money every month for savings.

2. Create a Realistic Budget

Create a budget that appropriately accounts for your earnings and expenses. Keep track of your expenditures to find places where you may make savings and debt repayment allocations more. Make frequent adjustments to your budget by using applications or tools for budgeting.

3. Set Specific Financial Goals

Establish precise, measurable financial objectives, such as debt repayment, emergency fund accumulation, or vacation savings. To keep yourself inspired and monitor your development, break these objectives down into more manageable, deadline-driven tasks.

4. Prioritize Debt Repayment

Prioritize paying off high-interest debt, such as credit card debt. If you want to efficiently lower your debt load, think about implementing tactics like the avalanche approach, which pays off the highest-interest loans first, or the snowball method, which pays off the smallest debts first.

5. Monitor Your Credit Score

To maintain accuracy, review your credit report and score on a regular basis. You should also be aware of how your financial actions impact your credit. Correct any mistakes as soon as you see them, and try to raise your credit score by making on-time bill payments, lowering credit card balances, and avoiding fresh credit queries.

6. Practice Mindful Spending

Make thoughtful spending decisions by determining whether an item will meet your needs and financial objectives; before making non-essential purchases, determine whether you really need it or if there are less expensive alternatives; apply the “24-hour rule” to impulse purchases to give yourself time to think things through.

7. Build an Emergency Fund

Build up your emergency fund gradually to three to six months’ worth of living expenditures, starting small. You can manage unforeseen costs without using credit cards or loans if you have this safety net in place.

8. Invest Regularly

Include investing on a regular basis in your financial routine. Make contributions to retirement accounts such as an IRA or 401(k), and take into account other investing possibilities according to your financial objectives and risk tolerance. Even modest sums of consistent investment over time can compound and contribute to wealth accumulation.

9. Educate Yourself Continuously

By reading books, going to workshops, or keeping up with reliable financial news sources, you can stay knowledgeable about financial matters. Gaining more knowledge over time will assist you in improving your financial judgment and adjusting to shifting market conditions.

10. Review and Adjust Regularly

Review your investing plan, budget, and financial goals on a regular basis to make sure they still fit your aims and living circumstances. As income, spending, or financial priorities change, make the necessary adjustments.

3.3 The role of discipline and self-control in achieving financial stability.

Having self-control and discipline is crucial to achieving financial security. They serve as the cornerstone around which sound financial practices are constructed, empowering you to consistently make deliberate choices that support your long-term objectives.

1. Maintaining a Budget

By controlling your spending in accordance with your financial strategy, discipline aids in budget compliance. Maintaining self-control is necessary to prevent impulsive purchases, prioritize needs over wants, and allocate funds for debt repayment, savings, and necessities.

2. Consistent Saving

It takes self-control to prioritize future financial security above instant enjoyment when saving on a regular basis. You can create a safety net and invest in long-term objectives like retirement, education, or housing by practicing discipline and regularly saving aside a percentage of your salary.

3. Debt Management

Effective debt management and reduction require disciplined behaviors such as paying bills on time, refraining from taking on needless debt, and paying more than the minimum amount owed. Maintaining self-control helps you avoid taking on more debt, which raises your credit score and improves your financial situation.

4. Delayed Gratification

Delaying gratification—postponing luxury or non-essential expenditures in favor of saving or investing—is frequently necessary to achieve financial security. By exercising self-control this helps you to focus on the greater picture and make present sacrifices that will pay off later.

5. Smart Investment Choices

Being a good investor means having the perseverance and self-control to stick with your plan through market ups and downs. Self-control enables you to adhere to a well-thought-out plan that is in line with your long-term financial goals rather than making rash investment decisions based on transient market fluctuations.

6. Adaptability to Change

Maintaining discipline also entails periodically assessing and modifying your financial plans in response to modifications in your life or financial situation. This flexibility, supported by self-control, guarantees that, despite obstacles, you stay on course to reach financial security.

3.4 Influence of attitudes, risk-taking, and mindset on money management.

Your financial decisions and results are influenced by your attitudes, risk tolerance, and mindset, which also define how you manage money. These variables affect not just the decisions you make but also the way you handle opportunities and difficulties related to money. Let’s see some key factors:

1. Attitudes towards Money

Your attitude towards money—whether you view it as a tool for freedom, security, status, or something else—greatly affects your financial behavior. For example: Having positive attitudes or negative attitudes money goes a long way in influencing your attitude towards money.

2. Risk-Taking and Investment Choices

Risk tolerance directly influences investment strategies and financial planning: Example: High risk Vs low risk; if you’re comfortable with taking high risk this makes you want to invest your money into things like startups, or other high-reward opportunities.

This could lead to significant growth, but also higher volatility and potential losses. On the other if you’re the such that is not comfortable in taking high risk, but wants to invest, you would prefer safer, more predictable investments like bonds or savings accounts, which provide stability but may offer lower returns over time.

3. Mindset and Financial Discipline

The passion for stretching yourself and sticking to it, even (or especially) when it’s not going well, is the hallmark of the growth mindset. –Carol Dweck. A growth-oriented mindset fosters resilience and adaptability, crucial for effective money management.

When you operate your personal finance from the stand point of growth, you’ll have the ability to view financial setbacks that may arise as learning opportunities. You become better equipped to lead more strategic adjustments and long-term planning. A growth mindset gives you the courage to continue learning about your finances and gives you the ability to come up with a proactive approach to building wealth.

On the other hand a fixed mindset believes that financial situations are static that deprives one to change spending habits, seek new opportunities, or recover from setbacks, limiting financial progress.

4. Short-Term vs. Long-Term Thinking

It’s no doubt that our mindset also affects whether we can focus on short-term gratification or long-term goals. In this regard short term thinking is a preference for immediate rewards that leads to impulsive spending, high debt levels, and insufficient savings. Why on the side is the long time thinking, this gives priority to future goals promotes disciplined saving, investing, and spending habits, leading to greater financial security and wealth accumulation over time.

5. Confidence in Financial Decision-Making

If you want to scale through financial turbulence, and make informed decisions then you need confidence; confidence is understanding and knowing how managing money affects your ability to make sound decisions.

Too much confidence which is also called high confidence leads to proactive management, such as seeking investment opportunities or negotiating better deals. The inability to carry out quick action is engineered by ones low confidence that results into inaction, missed opportunities, or reliance on others for financial decisions, which might not always align with ones best interests.

3.5 How habits and routines shape personal finance

Daily financial behaviors and long-term results are shaped by routines and habits, which are important factors in personal finance. Your capacity to realize your goals and achieve financial stability can be determined by the discipline and consistency of your financial habits.

1. Budgeting and Expense Tracking

Establishing fundamental routines such as tracking costs and creating a budget will help you gain insight into your financial situation. You can spot areas for improvement, prevent overpaying, and make sure you stick to your budget by making it a habit to check your expenditure. Maintaining a regular tracking schedule also aids in financial decision-making and future spending planning.

2. Saving and Investing

A solid financial foundation is created by making it a habit to invest and set aside a percentage of your income. Automated savings programs guarantee that you constantly contribute to your financial goals without the temptation to spend the money elsewhere. They work by automatically transferring a predetermined amount to savings or investment accounts each month. This practice aids in long-term wealth accumulation and needs planning.

3. Debt Management

Regularly making payments on debt, such as credit cards or loans, and following a strategy to reduce debt are vital financial habits. You can dramatically lower your total debt burden and enhance your financial health by making it a habit to pay more than the minimum amount owed and to prioritize paying off high-interest debt. This methodical strategy keeps your credit score high and helps you avoid paying needless interest.

4. Financial Review and Planning

Being aware of your financial condition requires regular planning sessions and reviews. You can stay on track by routinely evaluating your financial goals, checking your budget, and making necessary adjustments to your plans in response to shifts in income or spending. By being proactive, you may deal with problems before they become bigger problems and change your financial plan with knowledge.

5. Expense Awareness and Mindful Spending

You can make more thoughtful purchasing decisions if you develop habits connected to expense awareness and mindful spending. Intentional spending is encouraged by routinely assessing each expense to see if it fits with your values and financial goals. This practice guarantees that your spending is in line with your priorities and helps prevent impulsive purchases.

6. Emergency Preparedness

To ensure financial stability, one must consistently save and reload an emergency fund. Even little payments made on a regular basis to an emergency fund help you be ready for unforeseen costs or financial difficulties. During trying times, this practice acts as a safety net to lower stress and avoid financial issues.

4. FAQs on Behavior and Personal Finance

1. How does behavior affect personal finance?

Behavior affects debt management, investing, saving, and spending, which in turn affects one’s overall financial health.

2. Can changing behavior improve financial outcomes?

Certainly, improved financial growth and stability can result from forming responsible habits and making wise choices.

3. What are common behavioral traps to avoid?

Procrastination, impulsive spending, and failing to routinely save or create a budget are examples of common pitfalls.

4. How can seeking professional help benefit my financial well-being?

To maximize financial management and accomplish objectives, experts offer specialized counsel, tactics, and insights.

5. Where can I find resources to improve my financial habits?

Financial blogs, books, online courses, and financial advisor or coach consultations are examples of resources.

Let’s wrap up

Personal finance is greatly shaped by our behavior, which affects how we handle debt, investing, saving, and spending. Achieving and preserving financial stability requires an understanding of and commitment to improving financial behaviors. You may make better financial decisions and lay a strong foundation for your money by identifying and correcting behavioral patterns that impact your finances. Take proactive measures now to take charge of your financial future and work toward your long-term objectives, such as creating a budget, setting aside money on a regular basis, or consulting a professional.

Author: Bridget Austin

Ifeoma, who writes under the pen name Bridget Austin, is the founder of Inkwrit — a freelance writing platform built for African writers and storytellers. With a background in copywriting and content strategy, she created Inkwrit to give African voices a professional home to publish, build portfolios, and grow their writing careers. When she's not building the Inkwrit community, she writes about freelance writing, African literature, and the business of creative work.