Personal finance just like life insurance is something everyone should know about. I mean, if you work so hard to make your money, it is only right to know how to manage it. Also, personal finance is a part of everyone’s life. You handle money daily and have several things you settle with money like bills, paying your rent, groceries, etc. To do this without any stress, you must know how to plan your finances effectively to meet your needs and responsibilities.

What is Personal Finance and Why is it Important?

Personal finance is simply about planning and managing personal activities like income, spending, saving, investing, budgeting, etc. It’s all about managing your money and making it work for you, as well as meeting your financial goals (both short-term and long-term). Personal finance is not just about how much you make, but how you plan it, manage it, save it, and invest it.

Personal finance is very important because it is the road map towards achieving your financial goals. Financial goals can be something as big as saving for your children’s education or buying your dream house, or something as small as saving $20 monthly. Personal finance is just as the name says—personal. It is you making deliberate efforts to secure a financially free future. The first step is to figure out what you want to achieve and then set out money each month to achieve that goal.

Personal finance covers the following aspects of an individual’s life; budgeting, insurance, banking, investments, emergency planning, loans and mortgages, credit cards, and even taxes. It is not something you do once and forget about. It is a lifelong practice. This is because as we evolve as humans, our financial needs also keep changing. It is therefore wise to keep re-evaluating our financial goals through the years and adjust when we need to.

Focus Areas of Personal Finance

1. Income:

Income is the first component of personal finance. It is the total amount of money an individual earns monthly. To manage your finances, it is important to plan and make a budget for the money you earn. Financial planning involves allocating money for expenses, savings, and investments.

2. Spending:

The bulk of the income we earn goes into settling our numerous needs. Being able to manage our expenses is crucial to achieving our financial goals. We must ensure that we keep expenses lower than income. That way we don’t increase debts or mismanage our finances.

3. Saving:

Savings is that part of income left over after deducting expenses. Think of it as your financial umbrella. It is sometimes difficult to save with all the expenses we have, but we must strive to set something aside because it helps in times of emergencies and enables us to achieve our financial goals.

4. Investing:

This is where you make your money work for you. Savings shouldn’t be left idle but put in a place where it generates more money for you. Investments help money grow, increase wealth, and in the long run help you achieve your financial goals. You can invest in stocks, bonds, real estate, Treasury bills, etc.; however, you must be careful as some investments are risky.

5. Protection:

Protection here means safeguarding your wealth. It is putting aside money in plans that help you in times of unexpected events such as sickness, accidents, and even death. Some of such plans are insurance, emergency funds, and retirement plans.

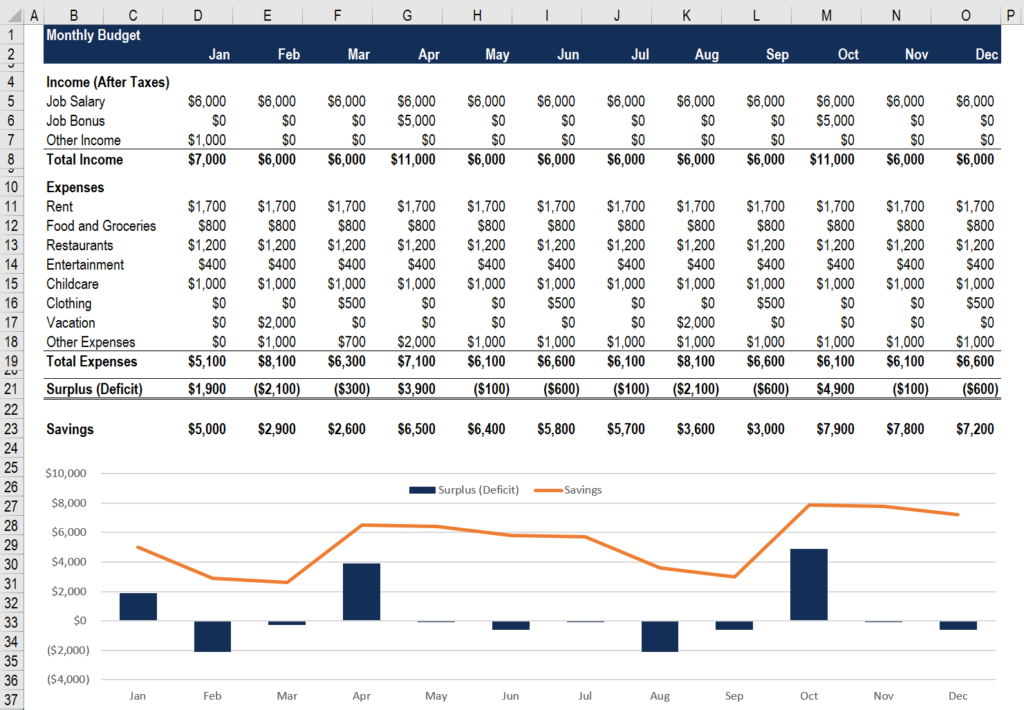

Example of a Personal Finance Budget

One of the best strategies to manage your money and move closer to your financial objectives is to create a personal finance budget. A carefully thought out budget can be your road map to financial success, whether you’re attempting to pay off debt, save for a major purchase, or just make sure you’re living within your means. This personal finance budget example is provided to help you visualize how you could divide your income into several categories so that you can better manage your money and keep tabs on your expenditures.

Why Personal Finance is Important

You might be wondering, Why should I bother myself about this? Here’s why?

1. Provides security:

Personal finance planning provides you with financial security and long-term protection. It’s not about how much money you have in your bank account, but knowing that you have enough to settle all your needs at all times.

2. Helps you achieve your financial goals:

The knowledge of personal finance enables you to achieve your financial goals. With the knowledge of smart investing, proper budgeting, saving strategies, and money management, you can build wealth and attain financial security.

3. Prepares you for emergencies:

Life is full of uncertainties. Having an emergency fund helps prepare you to be financially ready for whatever the future holds without you having to stress yourself. It provides you with a financial cushion to withstand all the troubles that might come your way.

4. Helps you make informed decisions:

A good understanding of personal finance assists you in making informed decisions about your money. Whether it is the right investment or saving plan, what debt to settle first, or choosing the right mortgage, being financially sound assists you in making decisions that align with your goals.

5. Reduces stress and anxiety:

One of the major sources of stress people face is as a result of money problems. They are constantly plagued with thoughts about paying bills or settling their debts, which eventually take a toll on their physical and mental health. Personal finance planning can reduce your stress and anxiety levels by giving you control of your money.

Essential Personal Finance skills

Budgeting and tracking expenses:

To win financially, you need to keep charge of your finances. Budgeting is a practical way to keep track of your expenses while pursuing your long-term goals. You can do that by creating a budget for your monthly income where every dollar has a job. Then track every single expense you make throughout the month. Having a budget enables you to make better choices and worry less about overspending or debts.

Saving and investing:

When it comes to building wealth, saving and investing are partners. Aim to save at least 20% of your monthly income. Start by having an emergency fund with three to six months’ worth of common expenses in it that can serve as a safety net in times of emergencies. Once you’ve done this, it’s time to invest. Money should not be left sitting idle in a savings account but put to work. Money invested compounds over time and also allows you to keep pace with inflation.

Managing debts:

Learning to manage debts helps maintain your financial health and stability. It involves tracking and controlling debts, making payments on time, and making informed decisions about borrowing and repayment. When it comes to debt repayment, consider paying high-interest debts first.

Common Personal Finance Mistakes

Whether you are or are not facing financial difficulties, steering clear of these mistakes can prove beneficial. They are:

i) Excessivee and frivolous spending: It may not feel like a big deal when you buy that dress you don’t need or order that extra package after eating out, but every little item adds up. Great fortunes are often lost one dollar at a time.

ii) Not investing in retirement: making monthly contributions to a designated retirement account helps for a comfortable retirement. If you don’t invest in a retirement plan, you’ll have nothing to fall back on when you finally retire.

iii) Not having a plan: you need to make setting aside some time to plan your finances a priority. You need to know where you are going. Your financial future depends on what is going on with you right now.

iv) Living on borrowed money: You need to cut expenses and keep it lower than your income. Living on borrowed money will accumulate debts over time and make you unable to attain financial freedom or reach your financial goal

v) Neglecting emergency funds: not investing in an emergency fund makes you vulnerable in times of financial crisis. It will also lead you to borrow money to meet those unplanned needs.

vi) No insurance policy: not investing in an insurance policy leaves you unprotected in times of uncertainty. It allows all your hard work to go to waste.

Creating a Successful Financial Plan

Now that you know and understand what personal finance is and its importance, here’s how you go about creating a successful financial plan.

i) Set financial goals: start by identifying and setting your financial goals. You can identify them as short-, mid-, or long-term goals. Whatever your goals are, ensure that they are specific and measurable. Instead of “I want to be better with money,” try “I want to save $20 monthly.

ii) Have a budget: a budget directs your finances. It tells you what is coming in (income), what’s going out (expenses), and what is being kept (savings). Start by tracking your spending and categorizing your expenses. This will tell where each dollar is going and where to cut back.

iii) Create an emergency fund: life is full of uncertainties. An emergency fund serves as a safety net in times of financial crisis. It comprises about three to six months of your living expenses, which will save you for dipping into your savings when unexpected needs aris

iv) Find different investment options: diversifyinvestmentsbased on your goals and financial data. Gather different investment options and invest accordingly.

v) Plan for retirement: retirement may still seem too far away, but it’s never too early to start planning. Start putting something aside in a retirement account. This way, when you grow old, you won’t have to depend on your children for your every need.

vi) Protect your assets: don’t let all your hard work be in vain. Protect your assets through diversification, insurance, and estate planning. Consider annuities and life, disability, and long-term insurance to safeguard against unexpected occurrences in your family, health, and life in general.

Conclusion

Personal finance can help you secure a financially secure life. Understanding how to manage your finances is an essential life hack that can help you live life without debt, gain control of financial stresses, and manage the uncertainties life throws at us. Remember, personal finance is a journey and not a destination. So start small, stay consistent, and watch how your small efforts compound into significant progress.

Notice of Disclaimer:

This article’s content is only meant to be used as general information; it is not intended to be financial advice. Because it is based on research and personal opinions, the content might not be appropriate for all readers. It is advised that you speak with a licensed financial advisor or other professional who can evaluate your unique situation and needs before making any financial decisions. Any financial loss or harm resulting from reliance on the information contained in this article is not the responsibility of the author or publisher. It is advised that readers do their own research and proceed with caution when making financial decisions.